With the 2026 IRCC proof of funds thresholds reaching new heights and refusal rates climbing to 18% for inadequate financial documentation, demonstrating sufficient settlement funds has never been more critical for Canadian immigration applicants. Proof of funds represents your ability to support yourself and your family in Canada without relying on social assistance, serving as a cornerstone requirement that can make or break your immigration journey.

This comprehensive guide delivers everything you need to navigate the complex proof of funds process successfully, from understanding updated 2026 requirements to avoiding common pitfalls that trigger refusals. We’ll focus primarily on Express Entry applications while covering important exemptions and alternative pathways that may apply to your situation.

What Are IRCC Proof of Funds and Why They Matter

IRCC proof of funds requirements exist to ensure immigrants can establish themselves in Canada without becoming a burden on the social safety net. These financial requirements demonstrate your capacity for self-support during the initial settlement period when you may not have immediate employment or income sources.

The scrutiny applied to proof of funds documentation has intensified significantly, with IRCC officers examining not just the amount of funds but their stability, accessibility, and legitimate source. Officers look for consistent account histories, proper documentation trails, and clear evidence that funds can be transferred to Canada when needed.

Key Principles: Available and Transferable Funds

Understanding what constitutes acceptable proof of funds requires grasping several fundamental principles that guide IRCC’s assessment process. These criteria determine whether your financial documentation will pass the rigorous review process.

- Funds must be readily available and accessible to you without restrictions or waiting periods

- Money must be transferable to Canada through legitimate banking channels without government restrictions

- Borrowed funds, including loans secured against assets, are strictly prohibited and will result in refusal

- Property equity, investments requiring liquidation, or frozen assets cannot count toward requirements

- Funds must be maintained consistently for at least six months prior to application submission

- Joint accounts are acceptable only if you can prove legal access and withdrawal rights

Consequences of Insufficient or Questionable Funds

Applications with inadequate or suspicious proof of funds face automatic refusal, with current statistics showing that 18% of Express Entry rejections stem from financial documentation issues. These refusals often require extensive reapplication processes that can delay your immigration timeline by 12-18 months.

Beyond immediate refusal, questionable financial documentation can raise red flags that affect future applications, requiring additional scrutiny and documentation to overcome previous concerns. The reputational impact extends to your entire application profile, making subsequent submissions more challenging to approve.

Who Needs Proof of Funds: Exemptions Explained

While proof of funds represents a standard requirement for most economic immigration programs, several important exemptions exist that can eliminate this obligation entirely. Understanding these exemptions can save significant time and documentation efforts for eligible applicants.

- Federal Skilled Worker Program (FSWP) applicants must provide proof of funds unless exempt through job offer

- Federal Skilled Trades Program (FSTP) candidates require financial documentation for themselves and dependents

- Provincial Nominee Programs (PNPs) typically mandate proof of funds with province-specific variations

- Canadian Experience Class (CEC) applicants are completely exempt from proof of funds requirements

- Applicants with arranged employment offers supported by positive Labour Market Impact Assessments are exempt

- Quebec-selected skilled workers follow separate financial requirements under Quebec immigration programs

- Protected persons and their dependents receive automatic exemption from financial requirements

How to Handle Exemption Documentation

Even when exempt from proof of funds requirements, applicants should prepare documentation explaining their exemption status, as the Express Entry system may still prompt for financial information. Upload a clear explanation letter detailing your exemption category and supporting evidence such as job offer letters or CEC eligibility confirmation.

This proactive approach prevents processing delays and demonstrates thorough preparation to reviewing officers. Include references to specific IRCC policy sections that support your exemption claim to strengthen your documentation package.

2026 Updated Proof of Funds Amounts by Family Size

The 2026 proof of funds requirements reflect updated Low Income Cut-Off (LICO) calculations, with amounts increasing substantially across all family sizes to account for inflation and rising living costs in major Canadian centers.

| Family Size | Minimum Funds (CAD) | Notes |

|---|---|---|

| 1 person (principal applicant) | $14,690 | Single applicant baseline |

| 2 people | $18,288 | Spouse or one dependent |

| 3 people | $22,483 | Family with one child |

| 4 people | $27,297 | Two children or dependents |

| 5 people | $30,976 | Three children or dependents |

| 6 people | $34,949 | Four children or dependents |

| 7 people | $38,922 | Five children or dependents |

| Each additional person | +$3,973 | Add for 8+ family members |

How IRCC Calculates Your Required Amount

Family size calculations include all dependent family members, regardless of whether they plan to accompany you to Canada initially. This encompasses your spouse or common-law partner, dependent children under 22, and any dependent children 22 or older with physical or mental conditions preventing self-support.

The Express Entry system automatically calculates your required amount based on family information provided in your profile. Updates to family composition require immediate profile updates to ensure accurate fund requirements throughout the process.

Maintaining Funds Until Visa Issuance

- Monitor account balances weekly to ensure they never drop below required thresholds during processing

- Update your Express Entry profile within 90 days if fund requirements change due to family composition updates

- Maintain funds in the same accounts used for documentation to preserve consistency and traceability

- Account for currency fluctuations if holding funds in non-Canadian dollars by maintaining additional buffer amounts

- Prepare to provide updated bank letters if requested during application processing stages

Step-by-Step: Acceptable Proof of Funds Documents

Gathering proper proof of funds documentation requires systematic preparation and attention to specific IRCC formatting requirements. The documentation process involves multiple components that must work together to create a convincing financial picture.

- Request official bank letters from all financial institutions holding your settlement funds

- Gather six months of bank statements showing consistent balance maintenance above required thresholds

- Collect gift documentation including signed letters and bank transfer records if applicable

- Prepare currency conversion documentation if funds are held in non-Canadian currencies

- Organize proof of funds transfer capability from your country to Canada through official banking channels

- Compile debt documentation or statements confirming no outstanding loans against settlement funds

- Create a summary document explaining your fund sources and organization for easy officer review

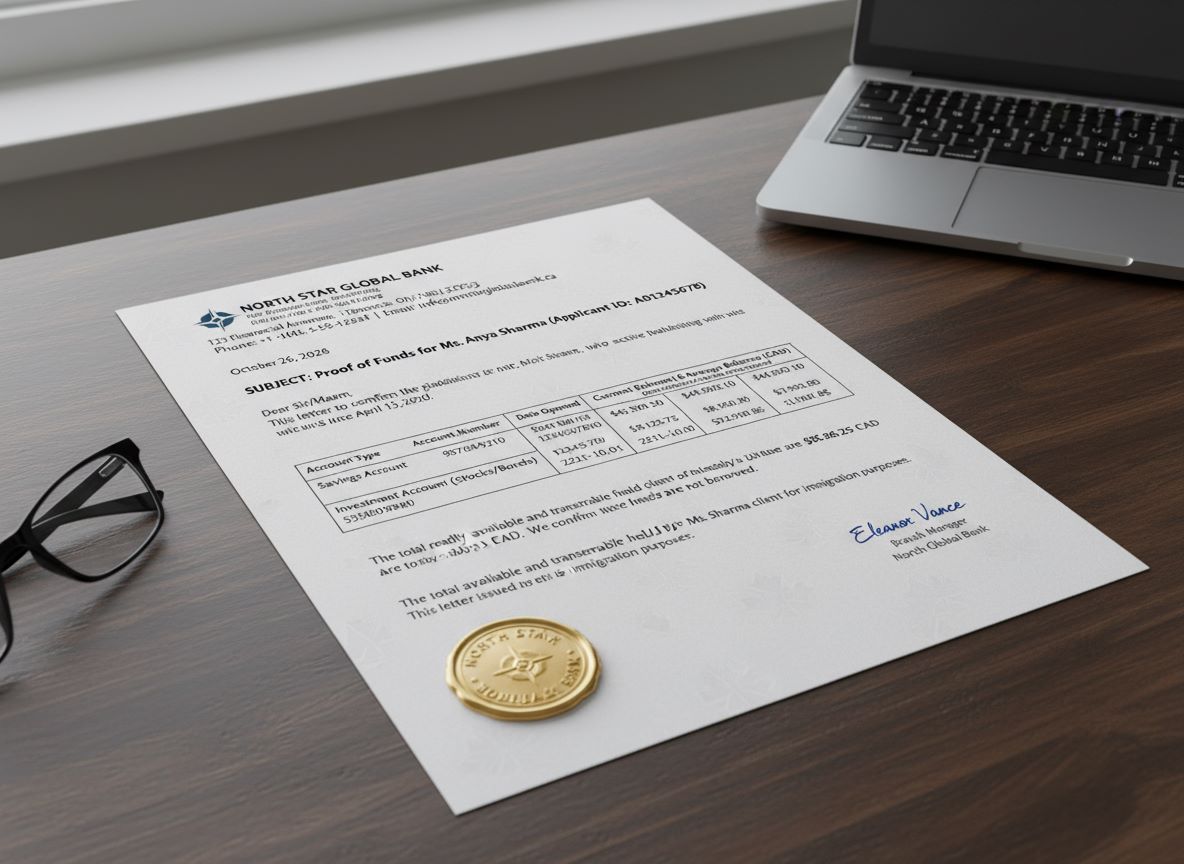

Official Bank Letter Requirements

Bank letters serve as the primary proof of funds document and must meet strict IRCC formatting and content requirements. These letters provide official confirmation of your financial standing and fund availability.

| Required Element | IRCC Specification | Common Mistakes |

|---|---|---|

| Bank letterhead and contact information | Official letterhead with phone, address, email | Using account statements instead |

| Account holder identification | Full name matching passport exactly | Name variations or nicknames |

| Outstanding debts and liabilities | Statement confirming no loans against funds | Omitting debt information |

| Six-month balance history | Monthly average balances for 6 months | Only current balance provided |

| Account opening date | Date when account was first opened | Recently opened accounts flagged |

| Bank officer signature and stamp | Authorized signature with official seal | Unsigned or unstamped letters |

| Currency and amount specifications | Clear currency designation and amounts | Ambiguous currency references |

Using Gifts, Loans, and Third-Party Funds

Gift funds from family members represent an acceptable source of settlement funds, provided they come with proper documentation demonstrating the funds are truly gifted without repayment obligations. The gift documentation must create a clear paper trail from the donor’s account to your settlement fund account, with signed legal declarations confirming the gift nature.

Borrowed funds remain strictly prohibited regardless of the source, including loans from family members, secured loans against property, or any arrangement requiring future repayment. Joint accounts with spouses or family members are acceptable if you can demonstrate legal access and withdrawal rights without requiring additional signatures or permissions.

Gift Documentation Checklist

- Signed and notarized gift letter from donor stating no repayment expectation and gift purpose for Canadian immigration

- Bank transfer records showing movement of funds from donor’s account to your settlement fund account

- Donor’s bank statement proving they possessed the gifted amount before transfer

- Proof of relationship between donor and recipient through birth certificates or marriage certificates

- Currency conversion documentation if gift involves international transfer between different currencies

- Legal declaration that gift funds do not originate from borrowed sources or illegal activities

Joint Accounts and Spouse Funds

Joint accounts require additional documentation proving your legal access to funds without restrictions from other account holders. This includes signed statements from joint account holders confirming your right to use funds for immigration purposes and bank confirmation that you can withdraw funds independently.

Spouse funds in separate accounts can support your proof of funds requirement when accompanied by a signed statement from your spouse authorizing use of their funds for family immigration settlement. Include marriage certificates or common-law relationship proof to establish the legal basis for shared financial resources.

Common Red Flags That Trigger IRCC Refusals

Understanding common proof of funds red flags helps applicants avoid documentation mistakes that frequently lead to application refusals. These issues often stem from attempts to manipulate account balances or inadequate documentation of legitimate fund sources.

| Issue | Why It Fails | Fix |

|---|---|---|

| Sudden large deposits before application | Suggests borrowed or temporary funds | Provide source documentation and wait 6 months |

| Newly opened bank accounts | Lacks stability and history demonstration | Use established accounts with longer history |

| Maintaining exactly minimum amounts | No buffer for currency fluctuations | Maintain 10-15% above requirements |

| Funds in countries with currency controls | Cannot prove transferability to Canada | Obtain government transfer authorization |

| Missing debt disclosure | Incomplete financial picture presentation | Declare all liabilities and outstanding loans |

| Inconsistent documentation dates | Suggests manipulation or coordination | Ensure all documents use consistent timing |

| Property sales timed to applications | Questions about fund permanence | Complete sales well before application |

| Unsigned or informal gift letters | Lacks legal validity and enforceability | Use notarized formal gift declarations |

Funds from Restricted Countries

Applicants from countries with currency controls or transfer restrictions must provide additional documentation proving their ability to move funds to Canada legally. This includes government authorization letters, central bank permissions, or official statements from authorized dealers confirming transfer capabilities within legal frameworks.

Consider opening accounts in countries without transfer restrictions or working with international banking partners to establish legitimate transfer mechanisms before applying. Some applicants successfully demonstrate transferability by moving smaller test amounts through official channels and documenting the process for IRCC review.

Step-by-Step Submission Process in Express Entry

The Express Entry submission process requires strategic timing and careful attention to system prompts and requirements throughout multiple stages from profile creation through final application submission.

- Enter accurate family size and fund amounts in initial Express Entry profile creation

- Upload proof of funds documentation within 90 days of receiving Invitation to Apply

- Organize documents according to IRCC file naming conventions and upload requirements

- Monitor profile for any requests for additional proof of funds documentation during processing

- Update fund amounts immediately if family composition changes affect requirements

- Maintain original fund levels until Confirmation of Permanent Residence issuance

- Prepare for possible interview requests if officers require clarification about fund sources

Document Organization Tips

- Use clear file names indicating document type and date: “BankLetter_Scotia_2026Jan15.pdf”

- Scan documents at 300 DPI minimum resolution with clear, readable text throughout

- Combine related documents into single PDFs when logical, such as bank letter plus statements

- Create cover letters explaining document organization and fund source summaries for complex cases

- Translate non-English documents using certified translators with appropriate certifications included

- Maintain backup copies of all submitted documents in organized digital and physical filing systems

Post-Submission Updates

After submission, monitor your application for any requests for updated proof of funds documentation, particularly if processing extends beyond six months and original bank letters become outdated. Respond promptly to any officer requests for clarification about fund sources, transfer capabilities, or family composition changes that affect requirements.

Advanced Tips for Bulletproof Proof of Funds

Creating bulletproof proof of funds documentation requires strategic planning beyond basic requirement compliance. These advanced strategies help ensure your application withstands the most rigorous scrutiny from experienced immigration officers.

| Strategy | Benefit | Implementation |

|---|---|---|

| Maintain 15-20% buffer above minimum | Protects against currency fluctuations | Calculate buffer based on currency volatility |

| Use multiple account diversification | Reduces single point of failure risk | Split funds across 2-3 established accounts |

| Professional document review | Catches errors before submission | Immigration lawyer or consultant review |

| Early fund consolidation | Establishes consistent account history | Move funds 8-12 months before applying |

| Comprehensive source documentation | Preempts officer questions about origins | Include salary, sale proceeds, gift papers |

| Currency hedging strategies | Locks in favorable exchange rates | Forward contracts or CAD conversions |

When to Consult an Immigration Professional

Complex proof of funds situations warrant professional consultation, particularly cases involving international gift transfers, funds from countries with banking restrictions, or mixed source documentation requiring careful presentation. Immigration professionals can review your specific circumstances and recommend strategies to present your financial situation in the strongest possible light.

Consider professional consultation if you’ve experienced previous refusals, have complex family financial arrangements, or need guidance on timing fund movements and applications for optimal success. The investment in professional review often prevents costly delays and refusals that can set back your immigration timeline significantly.